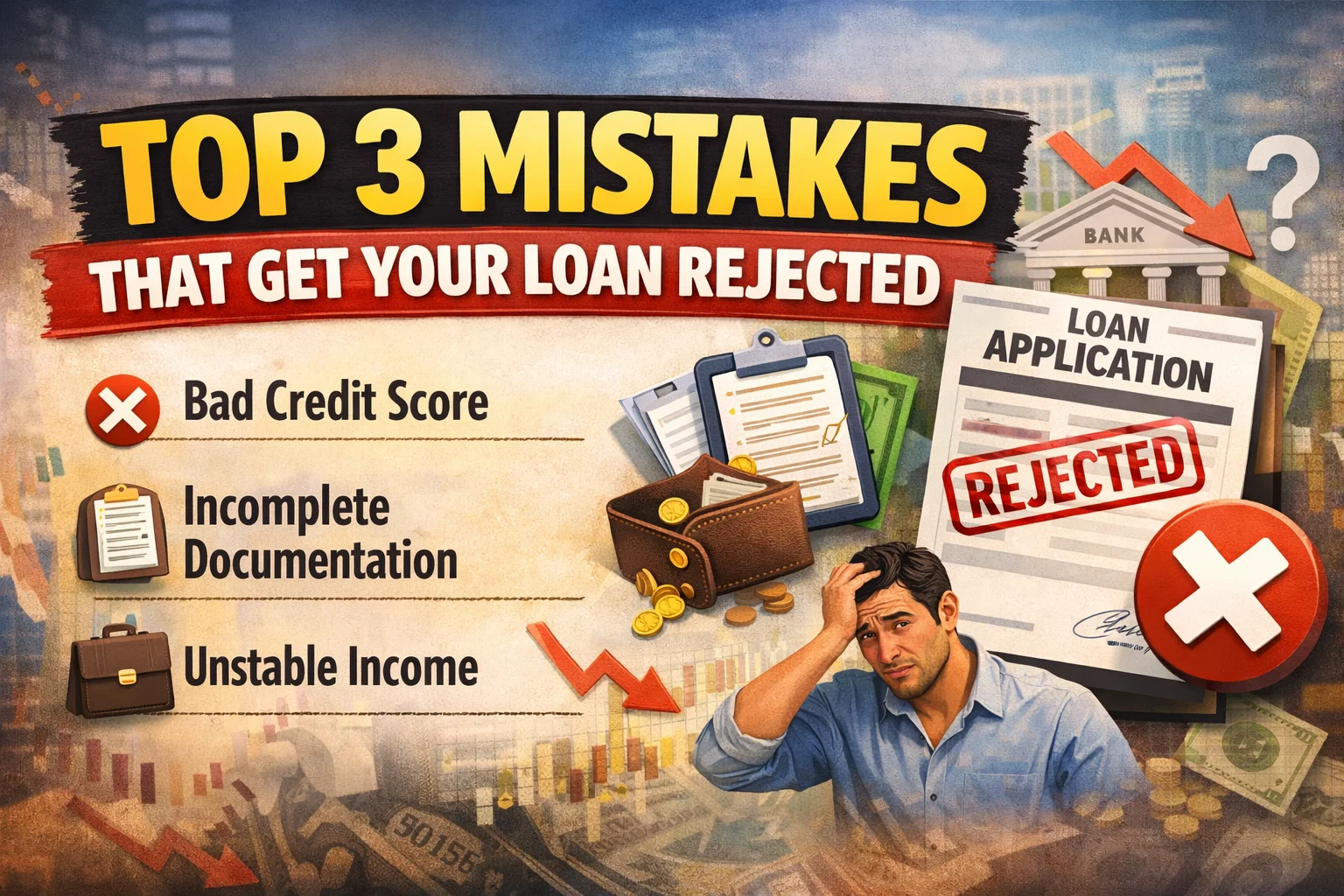

Getting your loan rejected can be frustrating, especially when you urgently need funds. In India, many personal loan, home loan, and business loan applications are rejected not because the applicant is ineligible, but due to common financial mistakes.

In this article, we explain the top 3 mistakes that get your loan rejected and how you can avoid them to improve your loan approval chances.

Why Do Banks Reject Loan Applications?

Banks and NBFCs evaluate your financial profile before approving a Online Personal Loan. Key factors include:

- CIBIL / Credit Score

- Income and employment stability

- Existing loan obligations

- Banking and repayment history

- Accuracy of documents submitted

Even one weak factor can lead to loan rejection.

1. Low or Poor Credit Score (CIBIL Score Below 700)

Your CIBIL score plays the most important role in loan approval. A score below 700 indicates high risk to lenders.

Why low credit score causes loan rejection

- Missed EMIs or late payments

- Credit card defaults

- High credit utilization

- Too many loan enquiries

How to improve your credit score

- Pay EMIs and credit card bills on time

- Keep credit usage below 30%

- Check your CIBIL report for errors

- Avoid applying for multiple loans at once

Tip: Even a single missed EMI can reduce your credit score significantly. You can apply for FD Against IDFC Credit Card.

2. High Existing Loan Burden (High FOIR)

FOIR (Fixed Obligation to Income Ratio) shows how much of your income already goes towards EMIs.

Why high FOIR leads to loan rejection

If your EMIs exceed 40–50% of your monthly income, banks consider it risky to approve another loan.

Example

If your monthly salary is ₹40,000 and your EMIs total ₹22,000, your FOIR becomes 55%, which can lead to rejection.

How to reduce FOIR

- Close small or high-interest loans

- Increase loan tenure to lower EMI

- Avoid unnecessary credit cards

- Apply for a realistic loan amount

3. Incorrect or Incomplete Documents

Many loan applications get rejected due to documentation errors, even when the applicant meets eligibility criteria.

Common document-related mistakes

- Name mismatch in PAN and Aadhaar

- Incorrect or outdated salary slips

- Incomplete bank statements

- Wrong employer or address details

- Submission of fake or edited documents

How to avoid document rejection

- Submit updated and genuine documents

- Ensure details match across all documents

- Double-check your loan application form

Other Mistakes That Can Get Your Loan Rejected

- Frequent job changes

- Applying immediately after joining a new job

- Poor banking history (cheque bounces)

- Applying for loan above eligibility

How to Increase Your Loan Approval Chances

- Maintain a CIBIL score above 700

- Keep EMIs within 50% of income

- Apply with accurate documents

- Choose the right lender for your profile

- Use a loan eligibility calculator

Final Thoughts

A loan rejection is not the end, it’s an opportunity to improve your financial profile. By avoiding these top 3 mistakes that get your loan rejected, you can increase approval chances and secure loans at better interest rates.

Before applying for a personal loan, home loan, or business loan, ensure your finances are well prepared.

Frequently Asked Questions (FAQs)

What is the minimum CIBIL score required for a loan?

Most banks prefer a CIBIL score of 700 or above for loan approval.

Does loan rejection affect credit score?

Loan rejection does not directly impact your credit score, but multiple loan applications do.

Can I get a loan with existing EMIs?

Yes, as long as your FOIR is within the acceptable range set by the lender.