The Indian government has introduced several schemes under the Pradhan Mantri Awas Yojana (PMAY) to make housing affordable for all. One such impactful initiative is the Credit Linked Subsidy Scheme (CLSS), which offers interest subsidies on home loans to different income groups—including the middle-income group (MIG). This article explores how CLSS benefits home loan borrowers in the middle-income segment, eligibility criteria, application procedures, and more.

What Is the Credit Linked Subsidy Scheme (CLSS)?

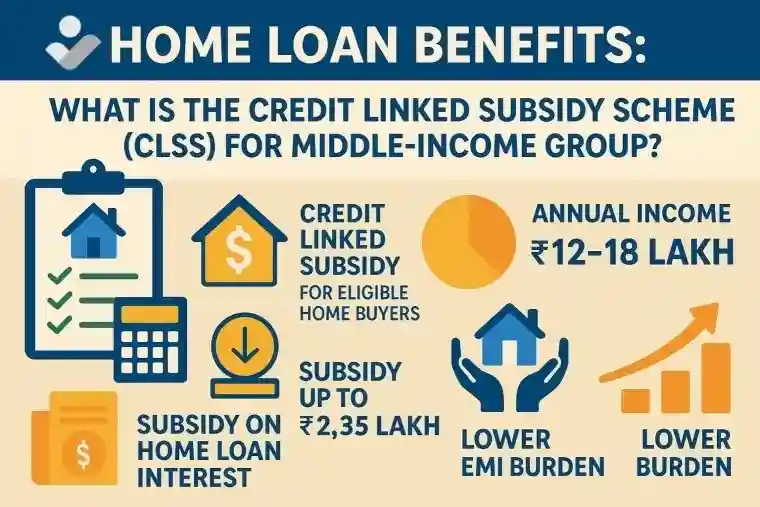

The Credit Linked Subsidy Scheme is a component of PMAY aimed at providing interest subsidies on home loans for the purchase, construction, extension, or improvement of a house. The scheme covers beneficiaries from Economically Weaker Sections (EWS), Lower Income Groups (LIG), and Middle-Income Groups (MIG-I and MIG-II).

CLSS for Middle-Income Group: An Overview

The CLSS for the middle-income group was introduced in 2017 to extend the benefits of affordable housing to those earning a modest but steady income. The subsidy under this scheme helps reduce the overall interest burden on the home loan, making housing more accessible.

- MIG-I: Households with an annual income between ₹6 lakh and ₹12 lakh

- MIG-II: Households with an annual income between ₹12 lakh and ₹18 lakh

Key Features of CLSS for MIG Home Loan Borrowers

Let’s understand the major features of the Credit Linked Subsidy Scheme for middle-income group:

Need Help Finding the Right Home Loan?

Bankstore.in can help you:

- ✔Get Home Loan Benefits at minimum rates

- ✔100% online process

- ✔ Free consultation & expert guidance

| Feature | MIG-I | MIG-II |

|---|---|---|

| Annual Income | ₹6–12 lakh | ₹12–18 lakh |

| Subsidy Rate | 4% | 3% |

| Loan Amount Eligible for Subsidy | ₹9 lakh | ₹12 lakh |

| Maximum Subsidy | ₹2.35 lakh approx. | ₹2.30 lakh approx. |

| Carpet Area Limit | Up to 160 sq.m | Up to 200 sq.m |

Eligibility Criteria for CLSS for Middle-Income Group

To avail of the CLSS subsidy on home loans, the applicant must fulfill the following eligibility criteria:

- The applicant must not own a pucca house anywhere in India in their name or in the name of any family member.

- The family should consist of husband, wife, and unmarried children.

- Income should fall within the MIG-I or MIG-II slab.

- The property should be in statutory towns as per the 2011 census or areas notified subsequently.

How Does the CLSS Interest Subsidy Work?

Under CLSS, the borrower receives a subsidy on the interest component of their home loan. This interest subsidy is calculated as a one-time upfront benefit and is credited directly to the borrower’s home loan account. It reduces the principal amount, thereby lowering the EMI.

For instance, if a person from MIG-I takes a home loan of ₹20 lakh, only ₹9 lakh is eligible for a 4% interest subsidy. The remaining amount does not qualify for the subsidy but can still be borrowed under standard loan terms.

Benefits of CLSS for Home Loan Borrowers

The home loan subsidy under CLSS offers several key advantages:

- Reduced EMIs: Lower principal due to the subsidy brings down monthly repayments.

- One-time Subsidy: No recurring paperwork; the benefit is adjusted upfront.

- Easy Process: Most major banks and NBFCs are CLSS partners under PMAY.

- Wider Accessibility: Middle-income families that were not eligible for previous affordable housing schemes now benefit.

How to Apply for CLSS Subsidy?

You can apply for the CLSS home loan subsidy through the following steps:

- Apply for a home loan at any bank or NBFC that is a PMAY lending institution.

- Submit your income proof and CLSS self-declaration form during the loan application.

- The lender verifies your eligibility and forwards your application to one of the Central Nodal Agencies (CNAs).

- Once approved, the subsidy amount is disbursed by the CNA and directly credited to your loan account.

Documents Required for CLSS under PMAY

Here is a list of important documents for claiming your CLSS home loan benefit:

- Income Proof (Form 16, Salary Slips, ITR)

- Aadhar Card of all family members

- Property Documents (Sale Agreement, Possession Letter)

- CLSS Self-declaration Affidavit

- Bank and Loan Account Details

CLSS Availability: Is It Still Active?

As of the last government update, the CLSS scheme for the MIG category ended on 31 March 2021. However, new housing schemes and extensions are frequently introduced in budget announcements. It’s advisable to check with your bank or visit the official PMAY website for the latest status.

Top Banks and Institutions Offering CLSS Home Loans

Several leading financial institutions offer CLSS-linked home loans. These include:

- State Bank of India (SBI)

- HDFC Ltd.

- ICICI Bank

- LIC Housing Finance

- Axis Bank

- PNB Housing Finance

Conclusion

If you belong to the middle-income group and are planning to buy your first home, the Credit Linked Subsidy Scheme for MIG is a valuable financial benefit that can ease your EMI burden. Even though the active window may have closed, staying informed and prepared can help you take advantage of future home loan subsidies under government schemes.

Always consult your lender and check the latest government notifications before proceeding with your home loan under CLSS. Owning your dream home might be more affordable than you think!